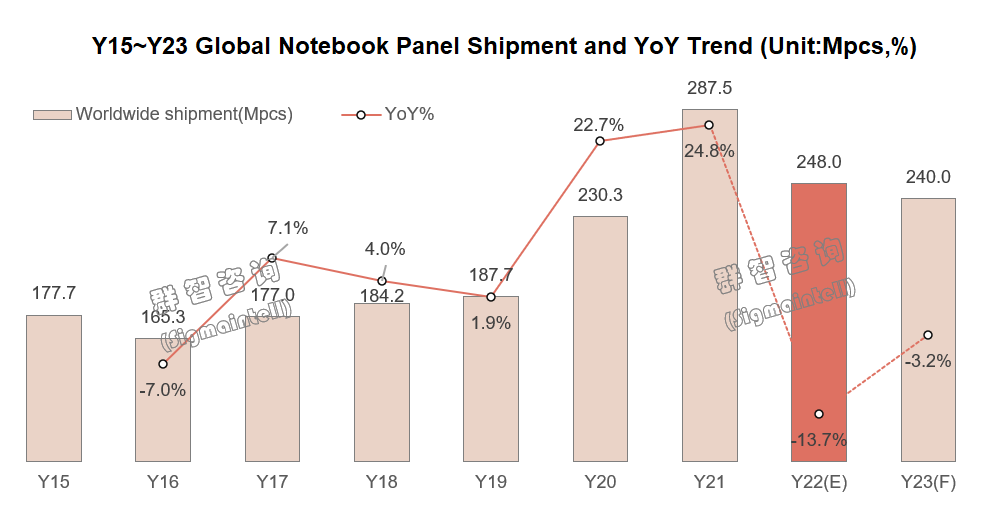

According to research data from Sigmaintell, the global shipment of notebook PC panel in 22Q1 was 70.3 million pieces, which decreased 9.3% from the peak in 21Q4; As the epidemic waned, the demand for overseas educational tenders has declined. In 2022, the demand for notebook PC enters a stage of rational development, and the scale of shipments drops in stages. However, the macro environment and geopolitical factors have exacerbated the degree of change, which is expected to bring short-term effects to the global supply chain of notebook computers supply. The mian notebook brands have accelerated their depurchasing strategies starting from the second quarter. Sigmaintell estimates that the global shipments of notebook panels in 22Q2 will be 57.9 million pieces, with a MoM decline of 17.7%.The total shipments are expected to be 248 million pieces in Y22, with a YoY decline of 13.7%.

Although the market has dropped significantly, the scale of overall shipment is still higher than the shipment level before the epidemic. At the same time, Sigmaintell believes that the long-term trend of product upgrades in the notebook market will remain unchanged and may accelerate after a brief adjustment, mainly reflected in the following areas:

Trend 1: The upgrade from 16:9 to 16:10 has become the mainstream trend

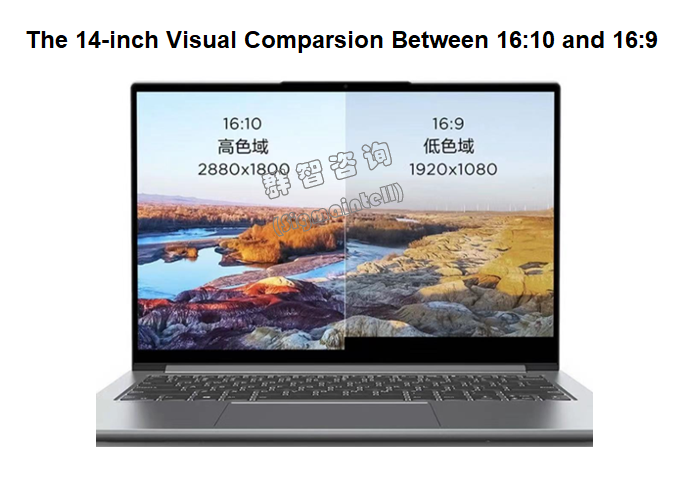

Like TV and monitor, the screen ratio of notebook was 4:3 in the early days and gradually developed to widescreen. In the past ten years, 16:9 has been the absolute main force of notebook panel. With the sharp increase in the office demand for ultrabook, consumers have put forward dual needs for office and entertainment, and the 16:10 screen is very close to the golden ratio of 1.618, which not only leads the 16:9 screen in the same size viewing area but also more comfortable in appearance. For example, compared with 14-inch 16:9, 14-inch 16:10 not only eliminates the "big chin" black frame and increases the viewing area by 10%. In 2019, panel makers successively received the brand’s 16:10 case-opening evaluation needs. With the mass production of new products, the set market promotion has achieved remarkable results, especially Lenovo’s Xiaoxin Pro 13. They lead the competition, and drove the 16:10 market popularity to increase continuously.

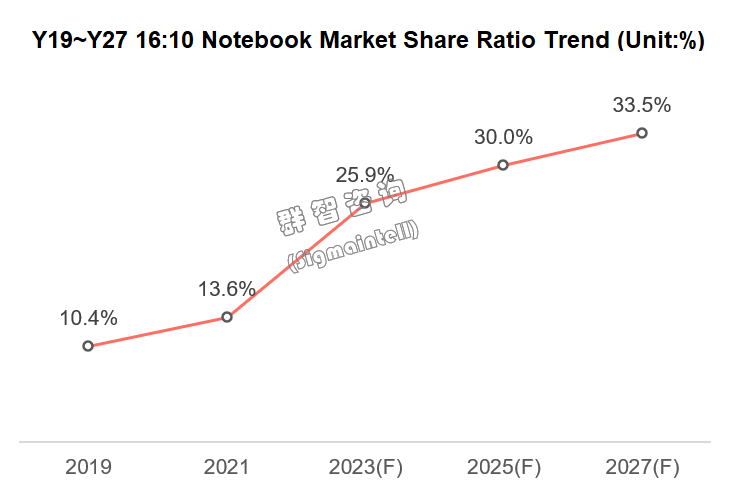

Sigmaintell believes that the penetration rate of 16:10 in the notebook market will gradually increase and become an important segment of the global notebook market. It is estimated that by 2027, the penetration rate of the 16:10 notebook market will reach 33.5%.

The 16:10 market penetration rate of the notebook market has increased rapidly, mainly due to these following reasons:

First, the market demand increases. First, the proportion of the 16:10 notebook display screen has increased significantly, and the vertical office display has increased, which is more in line with the trend of thin and light movement. Second, the "big chin" disappears; 16:10 is closer to the golden ratio, which contains a rich aesthetic value, and brings consumers a good sense of comfort and beauty. Third, the brand effect drove obviously. The 16:10 new product market represented by brands such as Apple, Lenovo, and Dell, has responded actively, leading to a substantial increase in demand on the supply chain.

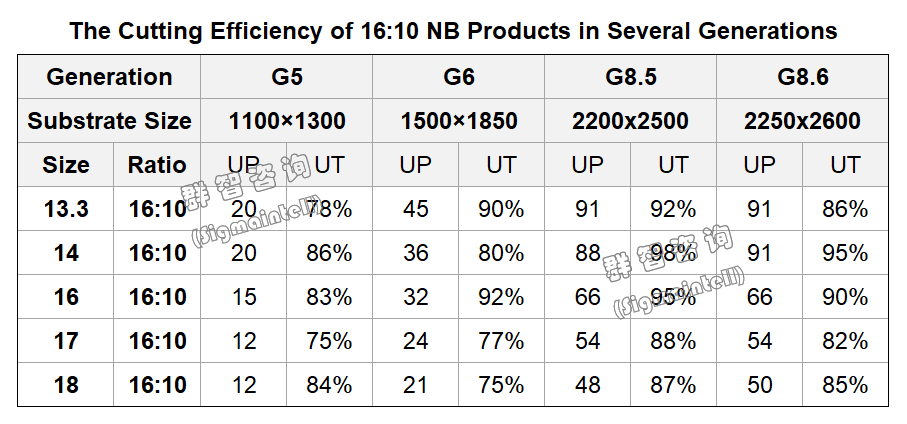

Second, the capacity of the large-generation line is gradually released.

Second, the capacity of the large-generation line is gradually released. As far as we know, between 2023 and 2026, it is expected that several IT-related large-generation lines will be mass-produced one after another. Among them, COST T9 G8.6 is scheduled to be mass-produced in 2023, and Tianma Xiamen G8.6 is designed to be mass-produced in 2024. What’s more, the SDC G8.5 OLED line is expected to be mass-produced in 2024, and IVO G8.6 and BOE Chengdu G8.6 OLED are also under the plan, that would be expected to be mass-produced from 2025 to 2026. In addition, Visionox is also planning the G8.6 OLED line. Compared with the small generation line (G5/G6), 16:10 product has higher cutting efficiency and has a significant cost advantage in large generation line (G8.5/G8.6). Therefore, the release of the large generation line's production capacity will help promote the scale of 16:10 product supply.

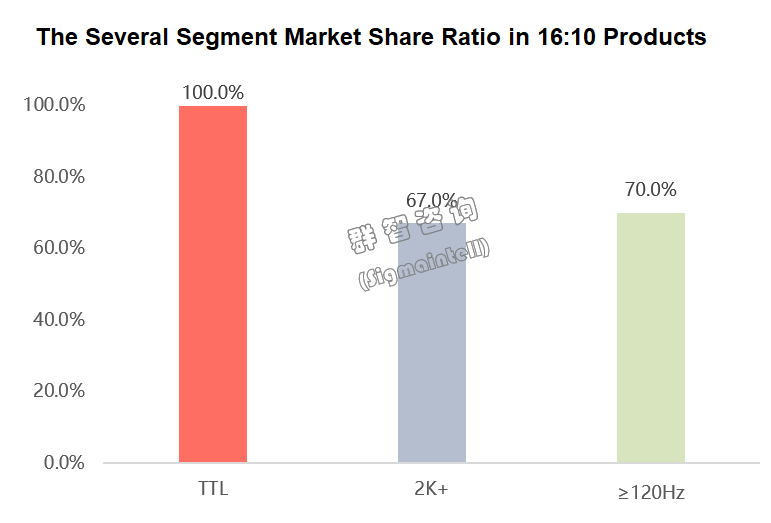

Third, compound growth demand. The 16:10 NB product is a composite type with market technologies such as high resolution and high refresh rate and has the driving force for continuous growth. In the NB roadmap of major panel makers in Y22~Y23, 16:10 new products accounted for 80.5%. Among them, the 2K+ high resolution market accounted for 67.0%, and the market of 120Hz and above accounted for 70.0%. BOE, INX, LGD, and CSOT’s 16:10 new product development is particularly active among the panel makers.

Therefore, according to a survey conducted by Sigmaintell, the 16:10 market has the following characteristics while developing rapidly:

First, the brand structure is still dominated by head brands. Head brands have robust brand premium capabilities and influence consumer habits and control over panel resources, which will be one step ahead in 16:10 product and market development.

Secondly, in terms of product specifications, it focuses on the positioning of mid and high-end products. The mainstream sizes are 14” and 16”, and the 16” 16:10 product will gradually occupy the 15.6” 16:9 market share. The resolution is concentrated in the 2K+ high resolution market, and the refresh rate is focused on 120Hz and above.

Next, new panel makers will usher in more opportunities. Due to the low cutting efficiency and high cost of 16:10 products in the small generation line, this hinders the development progress of 16:10 products by relevant panel makers to a certain extent. However, the commissioning of the new large-generation production line provides a stable capacity supply for 16:10 products and offers more opportunities for new panel makers such as CSOT and Tianma.

Trend 2: Resolution upgrade and refresh rate diversification are accelerating

As mentioned earlier, the development of new specifications for 16:10 is mainly focused on 2K+ high resolution and high refresh rate product specifications of 120Hz and above. Driven by 16:10, the penetration rate of high resolution and high refresh rate also increase gradually.

In addition to promoting the product side, another necessary driving force comes from consumers’ demand. With the rise of the hybrid office model, the office crowd have a strong demand for notebook performance upgrades, especially with the pile of high-performance ultrabook. While its market continues to expand, 2K~3K resolutions are favored by consumers. They have become a consumption hotspot, and major brands are competing for deployment. Taking Lenovo and ASUS as an example, in this year's new high-performance ultrabook, the resolution specification has been upgraded from 16:9 FHD to 16:10 2.5K, and the 12th generation CPU and RTX30 series high-performance GPU have been matched, significantly improving high-performance ultrabook’s specifications of office properties.

At the same time, the refresh-rate specification also broke through the attributes of e-sports and games for the first time and entered the main product line of high-performance ultrabook, which also led to the diversification of refresh-rate specifications, and this is mainly reflected in increased proportion in 120Hz and 165Hz in the high refresh-rate product line. The driving force behind is the expanding users’ base in the high refresh-rate notebook, which will also promote the continuous upgrade of the refresh rate in the next few years.

From the supply perspective, the panel manufacturing capacity and the wafer manufacturing capacity have gradually stepped out of shortage. The panel and IC supply chain have more resources and stronger motivation to support product development with high resolution and high refresh rate. According to the forecast data of Sigmaintell, in the global notebook panel shipments in 2022, the penetration rate of high resolution (2K+) will increase from 14.8% in 2021 to 20.6% in 2022; the penetration rate of high refresh rate (120Hz+) will increase from 6.5% in 2021 to 13.3% in 2022.

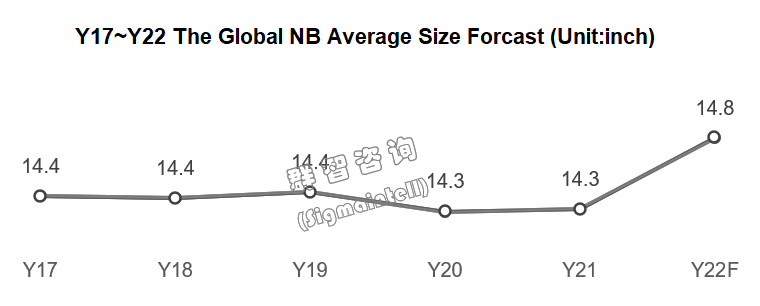

Trend 3: A combination of factors will drive the average size to a record high

Trend 3: A combination of factors will drive the average size to a record high

After the influence of the epidemic, the demands drive changes in new-forms revolution, resolution upgrade, and refresh-rate diversification, and these factors have jointly led to the growth of the average size of the notebook market and the increasing capacity of notebook panels intensifies competition in the notebook panel market. It further promotes the pace of panel makers to innovate and upgrade products. As a result, Sigmaintell forecasts that the average notebook panel size will break from 14.5 inches to 14.8 inches for the first time in 2022.

Under the influence of hyperinflation and the epidemic, the purchasing of set brands has slowed down in the short term, but the medium and long-term trends have not changed. Sigmaintell believes that the product upgrade speed of notebook will still accelerate after short-term adjustments. Therefore, Sigmaintell suggests that major panel makers need to actively adjust their product layouts according to market trends. At the same time, they need to strengthen their technical capacity reserves for panels such as high resolution and high refresh rate.

中文:

群智研究|全球笔电面板市场大盘回落 未改三大升级趋势

根据群智咨询(Sigmaintell)调研数据,2022年一季度全球笔记本电脑面板(Notebook PC Panel)出货量为7030万片,较2021年四季度高峰值下降9.3%;随着疫情带来的海外教育标案需求减退,2022年笔电的需求将进入理性发展阶段,出货规模呈现阶段性回落,但宏观环境和地缘政治因素加剧了这一变化程度,预计将给全球笔电供应链带来短期震动。二季度开始,笔记本电脑主力品牌加速去库存策略,群智咨询(Sigmaintell)预计,2022年二季度全球笔电面板出货将为5790万片,环比下滑幅度扩大至17.7%;2022年全年出货规模预计为2.48亿片,同比下降13.7%。

尽管大盘回落明显,但总体出货规模仍高于疫情前出货水平,同时,群智咨询(Sigmaintell)认为,笔电市场产品升级长期趋势不变,并在短暂调整后或将加快,主要体现在以下几方面:

趋势一:16:9向16:10升级成为主流趋势

与电视、显示器一样,笔记本电脑兴起初期屏幕比例都是4:3显示比例,并逐渐向宽屏发展,近十年16:9是笔记本电脑的绝对主力。随着轻薄本办公需求的急剧增加,消费者对办公与娱乐提出了双重需求,而16:10的屏幕非常接近1.618的黄金分割比例,不仅在同尺寸可视面积上领先16:9屏幕,而且观感上更加舒适。例如,14英寸16:10相较于14英寸16:9,不仅消除了“大下巴”黑框,可视面积亦增加了10%。2019年开始,面板厂商陆续接到品牌的16:10的开案评估需求,随着新产品量产,终端市场推广成效显著,特别是联想的新品小新pro 13上市后即销售大增并持续领先竞品,带动16:10市场热度不断增强。

群智咨询(Sigmaintell)认为,16:10在笔电市场的渗透率将逐步提升,成为全球笔记本电脑市场的一个重要细分市场,预计到2027年,16:10 NB市场渗透率将达到33.5%。

笔电市场16:10市场渗透率快速提升,主要有以下几方面原因:

第一,市场需求增加。其一,16:10笔记本显示屏占比提升明显,办公纵向显示更多,更符合轻薄化办公化趋势。其二,“大下巴”消失,16:10更贴近黄金比例,蕴含着丰富的美学价值,带给消费者良好的舒适感与美感。其三,品牌效应带动明显,以苹果、联想、戴尔等为代表品牌的16:10新品市场响应积极,亦带动供应链端需求大幅增加。

第二,大世代线产能逐渐释放。据了解,2023~2026年间,预计数条IT相关高世代线将陆续量产。其中,COST T9 G8.6预计2023年量产,天马厦门G8.6预计2024年量产,SDC G8.5 OLED线体预计2024年量产,IVO G8.6和BOE成都G8.6 OLED亦在规划之中,预计2025~2026年量产。除此之外,维信诺也在规划G8.6 OLED线体。相较于小世代线体(G5/G6),大世代线体(G8.5/G8.6)16:10产品切割效率更高,具备显著的成本优势。因此,大世代线产能的释放,将有助于推动16:10产品供应规模。

第三,复合式增长需求。16:10 NB产品是与高分辨率、高刷新率等市场技术的复合型,具备持续增长的动力。在各大面板厂商Y22~Y23的新品规划中,16:10新品占比80.5%。其中,2K+高分市场占比67.0%,120Hz及以上市场占比70.0%。在各面板厂表现中,BOE、INX、LGD、CSOT 16:10新品开发尤为积极。

因此,根据群智咨询(Sigmaintell)调查,16:10市场快速发展的同时,还具备以下特点:

首先,品牌格局仍以头部品牌为主。头部品牌拥有较强的品牌溢价能力,以及对消费者习惯的影响力和面板资源掌控能力,在16:10的产品和市场开拓中将领先一步。

其次,产品规格方面,集中在中高端产品定位。尺寸以14”和16”为市场主流,16” 16:10产品将逐步抢占15.6” 16:9市场份额。分辨率集中在2K+高分市场,刷新率集中在120Hz及以上。

再次,新进面板厂商将迎来更多机遇。因16:10产品在小世代线切割效率较低,成本较高,这在一定程度上阻碍了相关面板商16:10产品开发进度。但随着高世代新厂线的投产,为16:10产品提供了稳定的产能供应,也为CSOT、Tianma等新进面板厂商提供更多的机遇。

趋势二:分辨率升级刷新率多元化均加快

如前所述,16:10的新规格开发主要集中在2K+的高分辨率和120Hz及以上的高刷新率产品规格上,在16:10的推动下,高分和高刷的渗透率也随之提升。

除了产品端的推动,另一个重要的动力来自消费需求。随着混合办公模式(Hybrid-working model)的兴起,办公人群对笔记本性能升级有着强需求,特别表现在高性能轻薄本的兴起。在高性能轻薄本市场不断扩大的同时,2K~3K分辨率受到用户青睐,成为消费热点,主力品牌争相布局。以联想和华硕为例,在今年的高性能轻薄本新品中将分辨率规格从16:9 FHD升级到16:10 2.5K,并搭配12代CPU和RTX30系列高性能GPU,大幅提升了轻薄型笔记本的办公属性规格。

与此同时,刷新率规格也首次突破了电竞和游戏属性,进入高性能轻薄本的主力产品线,这也带动着刷新率规格走向多元化,主要表现在120Hz和165Hz在高刷产品线中占比提升。背后的动力则是高刷新率的用户群的扩大,这也将推动刷新率在未来数年的持续升级。

从供应来看,不论是面板产能还是晶圆制造产能,已经逐步走出了缺货的状态,面板及IC供应链均具备更多资源和更强动力来支持高分辨率和高刷新率的产品开发迭代。根据群智咨询(Sigmaintell)预测数据,2022年全球笔记本电脑面板出货中,高分辨率(2K+)渗透率将从2021年的14.8%增长到2022年的20.6%;高刷新率(120Hz+)渗透率将从2021年的6.5%增长到2022年的13.3%。

趋势三:综合因素推动平均尺寸将达历史新高

在经历疫情洗礼后,需求推动的新形态变革、分辨率升级和刷新率多元化共同催生了笔记本电脑市场平均尺寸的增长;而不断增加的笔记本面板产能正在使笔记本面板市场竞争加剧,竞争的加剧又进一步推动面板厂商创新和升级产品的步伐。因此,群智咨询(Sigmaintell)预测,笔记本电脑面板的平均尺寸将于2022年首次突破14.5英寸,来到14.8英寸。

尽管超级通胀和疫情因素的影响下,终端品牌面板备货短期减缓,但中长期趋势并未改变,群智咨询(Sigmaintell)认为,经过短期调整后,笔记本电脑面板的产品升级速度仍将加快。因此,群智咨询(Sigmaintell)建议,各大面板厂商需根据市场动态,积极调整产品布局,同时亦需加强对于高分、高刷等面板技术能力储备。